Cedar-IBSi FinTech Labs

Cedar-IBSi FinTech Labs

Analyst Briefings

Analyst Briefings

Get in touch

Get in touch

Back

Back

How is PSD2 protecting consumers online?

By Puja Sharma

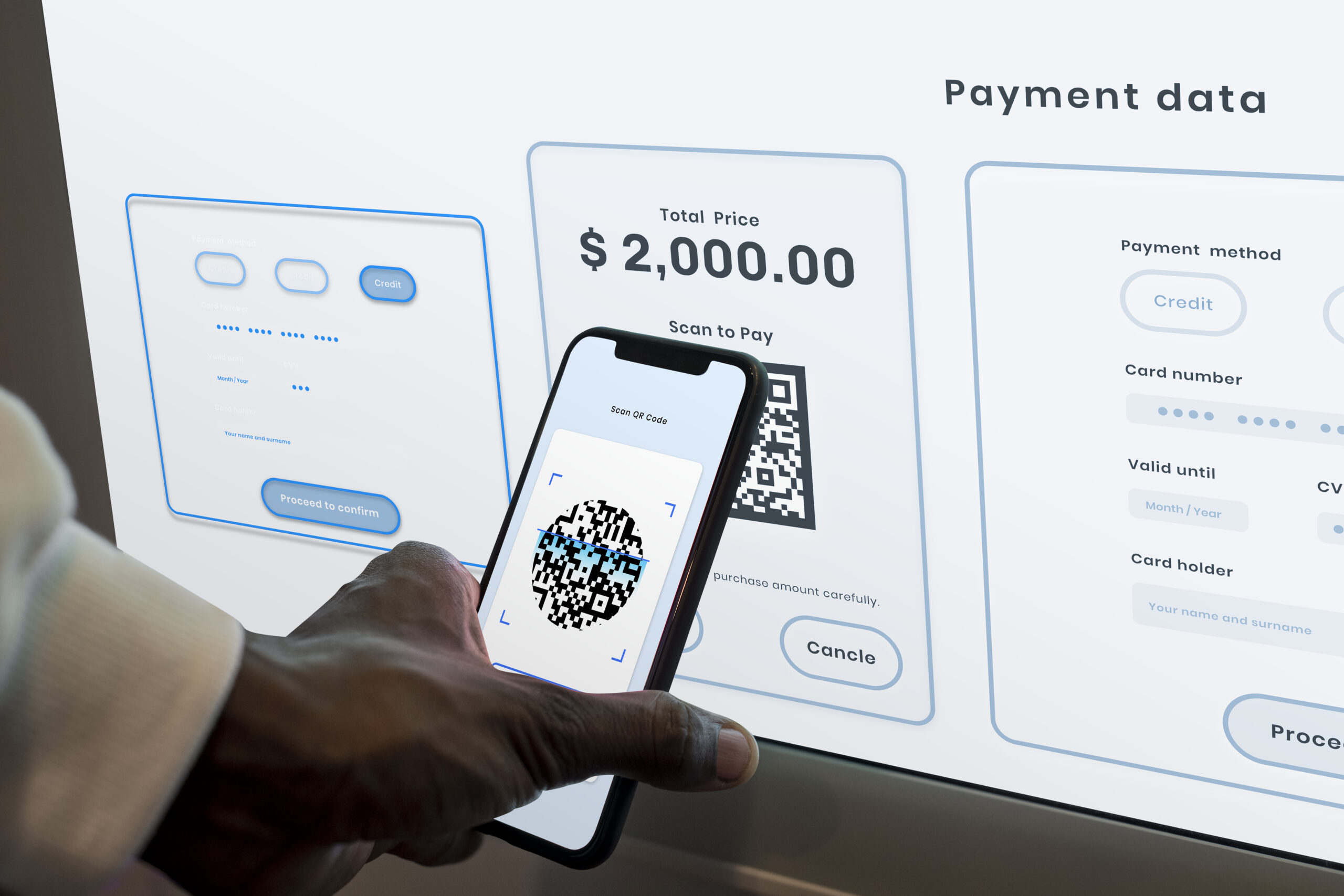

For e-commerce merchants, the most noticeable change of PSD2 is the introduction of Strong Customer Authentication. It is a process that requires customers to be assessed on their fraud risk level for purchases online. Those that are considered to have a risk of fraud are blocked from payments. However, legitimate customers still face difficulty in passing its tests.

The second Payment Services Directive (PSD2) came into force in January 2018, regulating payments across the EU and the UK. It aimed to create cohesive regulation for consumer protection and the rights and obligations of merchants and payment providers. However, as with any new regulation, compliance, and understanding what it means takes time. For online businesses, compliance with new fraud prevention processes has created difficulty. While compliance with PSD2 Strong Customer Authentication helps to avoid some fraud, it also has the potential to create poor customer experiences at the checkout, leading to fewer purchases.

However, as with any disruption, there are opportunities to be found where your competitors struggle. Compliance with PSD2 is not enough to secure your business’ future. Instead, you must understand the directive, its exemptions, difficulties, and benefits. Here, we explore how PSD2 has changed the eCommerce market and what can be done to boost your business and get ahead of your competitors.

What has PSD2 changed?

For eCommerce merchants, the most noticeable change of PSD2 is the introduction of Strong Customer Authentication (SCA). SCA is a process that requires customers to be assessed on their fraud risk level for purchases online. Those that are considered to have a risk of fraud are blocked from payments. However, legitimate customers still face difficulty in passing its tests.

SCA uses a two-factor identification. The process requires a consumer to prove two of three identity factors. These include knowledge, possession, and inherence. Or, to you and me, something we know, something we own, and something we are. So entering a password, using a mobile phone, or scanning a fingerprint can prove our identity.

However, by asking the customer to do this, SCA is creating touchpoints – processes that require action from the customer. This extends the checkout experience, taking away from the joy of a purchase. It doesn’t sound like a lot, but it has a deep impact. Merchants that use 3D-Secure 2.0 to verify customer identities for SCA (which is most merchants) should expect to lose 25% of their good orders, according to payments consultancy CMSPI. The efforts to protect consumers and merchants from fraud are causing more harm than it intends.

The market disruptor

But how can something that is supposed to benefit and protect businesses make them lose out on a quarter of their usual sales? Well, even the slight increase in touchpoints leads to increased negative customer experiences – shoppers, these days, favour efficiency and simplicity – and they can be unforgiving when things don’t go their way. Even then, SCA isn’t the most accurate; fraudsters can still sneak past defenses, and legitimate customers can be incorrectly blocked.

According to a consumer survey by Signifyd, negative checkout experiences are driving consumers into your competitors’ hands.

Around 30.6% of consumers said that multiple steps to verify their identity would be a reason why they wouldn’t shop with a specific online retailer again. Meanwhile, 57.6% said that they would not shop with an online retailer again if they had been declined for a purchase when there wasn’t a problem. While the decision of SCA may be out of your hands, consumers will direct the blame to the merchant.

The customer is always right, and it’s clear that SCA’s biggest disruption is with their experience. Building a positive brand image of reliability that encourages returning customers begins with your reliability at checkout. Only then can you get ahead of your competitors that are falling at the hurdles set out by PSD2 compliance.

New opportunities

PSD2 compliance alone isn’t sustainable for any proactive business. So, how do we get around the issues of SCA and negative customer experiences? Despite SCA’s disruption, some simple yet innovative fixes can help you find new opportunities within the world of eCommerce.

According to the Baymard Institute, 26% of consumers cited checkout processes being too long as a key reason for cart abandonment. We need to simplify the process and make it easier, especially with SCA. Diversifying payment options is one way to achieve this, and optimizing your site for mobile use can also be beneficial.

Their innovation secures data and makes it easier for consumers to shop online. Their verification process mainly uses inherence, meaning that a fingerprint scan or facial recognition can complete a purchase. By allowing consumers to use a mobile site, they’re also proving their possession of a phone. Already, the verification process has been made easier than it would’ve been on a desktop computer or laptop. Simplicity is the best solution, and it can make SCA easier.

Another way to reduce the friction caused by SCA identity verification is by using an intelligent commerce protection platform. By leveraging artificial intelligence and machine learning, these platforms can analyze the risk level of consumers based on a variety of factors, including their historic checkout behavior and purchasing choices. Consumers whose identities can be verified across multiple touchpoints and shopping history can be verified more quickly as part of SCA. This removes touchpoints from the checkout process and is also a more accurate measure to combat fraud and abuse. It works to prevent fraud by 100%.

Not only does this improve the customer experience, but by alleviating the cost of fraud and abuse, merchants can boost their revenue – an area where their competitors will be missing out.

While compliance with PSD2 proves the competence of a business to act on regulation, understanding the directive and how to navigate around it for the benefit of merchants and consumers alike is the sign of a true market leader. By identifying the problems of SCA, you can find solutions that your competitors have not even considered.

IBSi FinTech Journal

- Most trusted FinTech journal since 1991

- Digital monthly issue

- 60+ pages of research, analysis, interviews, opinions, and rankings

Other Related News

Related Reports

Sales League Table Report 2026

Know More

Global Digital Banking Market Landscape & Vendor Analysis Q2 2026

Know More

Wealth Management & Private Banking Systems Report Q4 2025

Know More

Incentive Compensation Management Report Q4 2025

Know More