Cedar-IBSi FinTech Labs

Cedar-IBSi FinTech Labs

Analyst Briefings

Analyst Briefings

Get in touch

Get in touch

Back

Back

How algorithmic trading powered by AI influences stock market liquidity

By Mehaan Doshi, Haileybury College

Abstract: Artificial intelligence has played a pivotal role in modern finance, revolutionizing the industry. From being able to analyze big data to executing complex trades, it has restructured the way in which all types of investors interact with the stock market. Liquidity, the ease at which an asset can be bought or sold without affecting the price, is a crucial aspect of the stock market, and financial institutions utilising AI for investment analysis and trading can definitely lead to an impact. This paper adopts a review of existing literature and academic research on relevant topics to investigate the impact of AI on stock market liquidity.

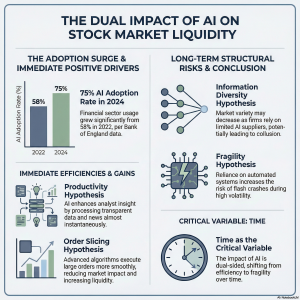

Introduction: Artificial Intelligence (AI) is the field of computer science that focuses on mimicking human intelligence and performing human tasks. The most prominent subset of AI is machine learning, which allows computers to make predictions by learning from data. Stock market liquidity is the ease of buying or selling stocks without impacting the share price. 1 According to a Bank of England survey, 75% of financial companies used AI in 2024, a substantial increase from 58% in 2022.

Cao and collaborators.(2023) showed 1 This is the website of the survey: that listed companies adjusted their corporate filings style and word choice in response to increasing AI application by investors. As many asset managers increasingly use AI in their investment analysis and trading, there could be systematic effects on stock market liquidity.

Asset managers, particularly hedge funds, are incentivized to utilize AI tools as it can increase profits in trading. Compared to simple models, complex models based on machine learning can predict stock returns with greater accuracy (Kelly, Malamud, and Zhou, 2024). Babina et al. (2024) found that AI increases productivity by boosting product innovation. Furthermore, AI outperforms human analysts at processing large quantities of transparent data, while human analysts are better positioned in tasks requiring institutional knowledge or where context is required, such as small, asset-light, or illiquid firms (Cao et al., 2024).

In practice, AI algorithms can support investment analysis and decision making, so that fund managers and financial analysts can use technologies such as Natural Language Processing (NLP) for textual analysis, Computer Vision (CV) for image recognition, and voice recognition algorithms. These tools allow financial professionals to process financial, political, and regulatory news almost instantaneously. For example, Gómez-Cram and Grotteria (2022) showed that textual analysis of the Federal Reserve meetings can predict foreign exchange futures and stock index returns. Traders can also use AI algorithms to predict short-term changes in stock prices and split up orders more smoothly, which can reduce market impact. Machine learning models have demonstrated a significant ability to improve investment returns. Gu, Kelly, and Xiu (2020) found that machine learning outperformed older regression models, and in some cases even doubled investment performance. This presents the idea that AI can improve the productive potential of asset managers by enabling better investment decisions.

Likewise, DeMiguel et al. (2023) showed that machine learning methods can identify mutual funds that consistently perform well, while Leippold, Wang, and Zhou (2022) found that machine learning can build predictive factors for stock returns. These findings suggest that AI allows for more accurate interpretations of market data. Chen and McCoy (2024) further supported this argument by conducting a study, using 159 return predictors powered by machine learning. They found that machine learning algorithms can still function effectively even when data is missing, using simple methods like mean imputation.

Additionally, Martin and Nagel (2022) argue that risk-neutral Bayesian investors can predict stock returns using observable characteristics, implying that AI algorithms can replicate this predictive power. Easley, López de Prado, O’Hara, and Zhang (2021) show that machine learning can increase the explanatory power of market microstructure measures, which are key in understanding liquidity. Firms with greater stock liquidity tend to have stronger performance (Fang, Noe, and Tice, 2009). This relationship is due to the improved information available from the stock price. Cartea et al. (2022) showed that liquidity providers can use reinforcement learning to dynamically assess and manage risk in financial markets.

This can increase their profitability and attract more liquidity providers, allowing AI to increase market efficiency by increasing their profits. Brogaard, J., Hendershott, T., & Riordan, R. (2014) found that high-frequency trading performed by AI can improve price efficiency by helping traders distinguish between permanent price and transitory pricing errors. Because AI is increasingly being integrated in high-frequency trading, this finding implies that AI-powered trading could enhance the efficiency of price discovery.

This can increase their profitability and attract more liquidity providers, allowing AI to increase market efficiency by increasing their profits. Brogaard, J., Hendershott, T., & Riordan, R. (2014) found that high-frequency trading performed by AI can improve price efficiency by helping traders distinguish between permanent price and transitory pricing errors. Because AI is increasingly being integrated in high-frequency trading, this finding implies that AI-powered trading could enhance the efficiency of price discovery.

Amihud, Mendelson, and Lauterbach (1997) analyzed how changes to trading mechanisms, specifically moving from daily call auctions to continuous trading, in the Tel Aviv Stock exchange affect stock prices. They found that it leads to a permanent increase in stock prices as well as enhancements in stock market liquidity and price efficiency.

Goyenko, Holden, and Trzcinka (2009) compared the different measures of liquidity and found that effective spread (how far the actual trade price is from the midpoint between the bid and ask spread at the time of trade) divided by realized spread (how far the trade price is from the midpoints a few minutes after a trade) is most effective, and that Amihud illiquidity measure captures price impact well. This measure is useful for assessing how trading practices influence market liquidity. However, studies have examined how AI driven trading and research may influence the quality and range of information available.

Dou et al. (2025) argue that AI-powered trading may reduce market efficiency because reinforcement learning can lead to collusion without explicit agreements among traders, raising concerns that it may reduce liquidity. However, Cartea et al. (2022) empirically showed that collusion by AI-powered traders is unlikely in moderate or highly competitive markets. Additionally, Farboodi and Veldkamp (2020) challenged the notion that increased use of technical trading reduces price informativeness by showing that, because of improvements in fintech, price informativeness doesn’t decrease even when more investors switch to technical analysis. Furthermore, several studies also suggest that AI utilization could lead to an increase in the fragility of financial markets.

For example, Kirilenko et al. (2017) studied the 2010 Flash Crash and found that high-frequency traders did not change their trading patterns at the beginning of the market crash. This implies that automated trading systems, often powered by AI, may not respond appropriately towards periods of high volatility. Shkilko and Sokolov (2020) add that the removal of fastest traders’ speed advantage reduces trading costs, implying that unequal access to AI tools may lead to high trading costs, which causes market fragility, as if some institutional investors have an advantage in using AI, while others don’t, trading costs and market fragility may increase in the long term.

Hypotheses: The previous analysis has helped me generate the following hypotheses:

- Productivity hypothesis : AI may increase stock market liquidity by enhancing fund managers, traders, and financial analysts’ productivity. AI can save fund managers’ time in processing transparent information, which may increase fund managers’ investment insight.

- Order slicing hypothesis : AI can slice up orders more smoothly than simple trading algorithms, which may increase liquidity. –

- Information diversity hypothesis: If all firms use AI technology from a limited number of suppliers, and if reinforcement learning leads to collusion among traders, then information production and diversity may decrease.

- Fragility hypothesis: AI can increase the fragility of the stock market so there may be more flash crashes.

Theoretical prediction: After reviewing the literature, I have come to the conclusion that there is a dual sided impact on stock market liquidity, in which time plays a critical role. In the short term, the Productivity hypothesis and Order Slicing hypothesis are likely to dominate. AI increases the speed and accuracy of investment decisions and improves execution of large orders by efficiently breaking them down.

This will overall increase stock market liquidity in a shorter timeframe In the long term, however, the risks of incorporating AI in trading can enhance the effects of the Information Diversity hypothesis and the Fragility hypothesis. Due to AI being more widely used in the future, the prominence of AI among asset managers will increase, leading to a reduction in diversity of information in the market. Furthermore, an elevated reliance on AI in stock market trading can leave the stock market in a very fragile position.

References:

Amihud, Y., Mendelson, H., & Lauterbach, B. (1997). Market microstructure and securities values: Evidence from the Tel Aviv Stock Exchange. Journal of Financial Economics, 45 (3) , 365-390.

Brogaard, J., Hendershott, T., & Riordan, R. (2014). High-frequency trading and price discovery. The Review of Financial Studies, 27(8), 2267-2306.

Cao, S., Jiang, W., Yang, B., & Zhang, A. L. (2023). How to talk when a machine is listening: Corporate disclosure in the age of AI. The Review of Financial Studies, 36 (9), 3603-3642. Cartea, Á., Chang, P., Mroczka, M., & Oomen, R. (2022). AI-driven liquidity provision in OTC financial markets.

Quantitative Finance, 22 (12), 2171-2204. Chen, A. Y., & McCoy, J. (2024). Missing values handling for machine learning portfolios. Journal of Financial Economics, 155 , 103815.

DeMiguel, V., Gil-Bazo, J., Nogales, F. J., & Santos, A. A. (2023). Machine learning and fund characteristics help to select mutual funds with positive alpha.

Journal of Financial Economics, 150 (3) , 103737. Dou, W. W., Goldstein, I., & Ji, Y. (2025). AI-powered trading, algorithmic collusion, and price efficiency. Jacobs Levy Equity Management Center for Quantitative Financial Research Paper, The Wharton School Research Paper. Easley, D., López de Prado, M., O’Hara, M., & Zhang, Z. (2021).

Microstructure in the machine age. The Review of Financial Studies, 34 (7), 3316-3363. Fang, V. W., Noe, T. H., & Tice, S. (2009). Stock market liquidity and firm value. Journal of Financial Economics, 94 (1), 150-169. Farboodi, M., & Veldkamp, L. (2020). Long-Run Growth of Financial Data Technology. American Economic Review, 110 , 2485–2523. Goldstein, I., Spatt, C. S., & Ye, M. (2021).

Big data in finance. The Review of Financial Studies, 34 (7), 3213-3225. Gómez-Cram, R., & Grotteria, M. (2022). Real-time price discovery via verbal communication: Method and application to Fedspeak.

Journal of Financial Economics, 143 (3), 993-1025. Goyenko, R. Y., Holden, C. W., & Trzcinka, C. A. (2009). Do liquidity measures measure liquidity?

Journal of Financial Economics, 92 (2), 153-181. Gu, S., Kelly, B., & Xiu, D. (2020).

Empirical asset pricing via machine learning. The Review of Financial Studies, 33 (5), 2223-2273. Kaniel, R., Lin, Z., Pelger, M., & Van Nieuwerburgh, S. (2023). Machine-learning the skill of mutual fund managers.Journal of Financial Economics, 150 (1), 94-138. Kelly, B., Malamud, S., & Zhou, K. (2024). The virtue of complexity in return prediction.

The Journal of Finance, 79 (1), 459-503. Kirilenko, A., Kyle, A. S., Samadi, M., & Tuzun, T. (2017). The flash crash: High-frequency trading in an electronic market. The Journal of Finance, 72(3), 967-998. Leippold, M., Wang, Q., & Zhou, W. (2022).

Machine learning in the Chinese stock market. Journal of Financial Economics, 145 (2), 64-82. Martin, I. W., & Nagel, S. (2022). Market efficiency in the age of big data. Journal of Financial Economics, 145 (1), 154-177. Obaid, K., & Pukthuanthong, K. (2022).

A picture is worth a thousand words: Measuring investor sentiment by combining machine learning and photos from news. Journal of Financial Economics, 144 (1), 273-297. Shkilko, A., & Sokolov, K. (2020). Every cloud has a silver lining: Fast trading, microwave connectivity, and trading costs. The Journal of Finance, 75 (6), 2899-2927.

IBSi News

Get the IBSi FinTech Journal India Edition

- Insightful Financial Technology News Analysis

- Leadership Interviews from the Indian FinTech Ecosystem

- Expert Perspectives from the Executive Team

- Snapshots of Industry Deals, Events & Insights

- An India FinTech Case Study

- Monthly issues of the iconic global IBSi FinTech Journal

- Attend a webinar hosted by the magazine once during your subscription period

₹200 ₹99*/month

* Discounted Offer for a Limited Period on a 12-month Subscription

IBSi FinTech Journal

- Most trusted FinTech journal since 1991

- Digital monthly issue

- 60+ pages of research, analysis, interviews, opinions, and rankings

Other Related Blogs

July 13, 2026