Cedar-IBSi FinTech Labs

Cedar-IBSi FinTech Labs

Analyst Briefings

Analyst Briefings

Get in touch

Get in touch

Back

Back

FinTech funding trends: Digital payments reign supreme in India, Neobanks and InsurTech on the rise

By Puja Sharma

In recent years, India has emerged as a hotbed of innovation and growth in the financial technology (FinTech) sector, fueled by a confluence of factors such as technological advancements, changing consumer preferences, and supportive regulatory measures.

In recent years, India has emerged as a hotbed of innovation and growth in the financial technology (FinTech) sector, fueled by a confluence of factors such as technological advancements, changing consumer preferences, and supportive regulatory measures.

As evidenced by the distribution of funding across various FinTech segments, the Indian market is witnessing a dynamic shift towards digitalization, with specific sectors experiencing particularly pronounced momentum.

Understanding these dynamics is not only essential for stakeholders seeking to capitalize on emerging opportunities but also holds profound implications for the future trajectory of India’s financial sector and its broader economic landscape.

As per data from IBS Intelligence, understanding these dynamics is not only essential for stakeholders seeking to capitalize on emerging opportunities but also holds profound implications for the future trajectory of India’s financial sector and its broader economic landscape.

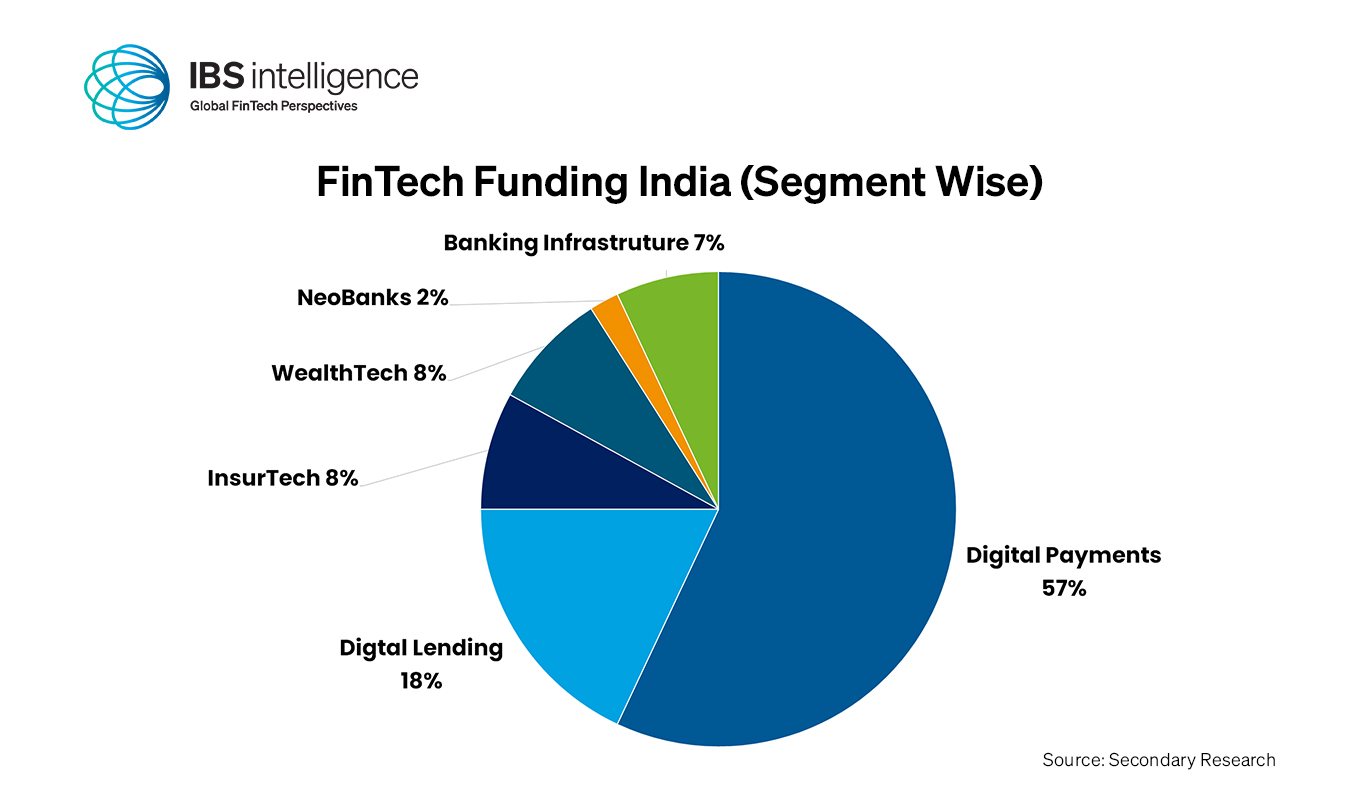

Banking Infrastructure (7%):

Investment in banking infrastructure is essential due to the increasing demand for digital banking services. Traditional banks are modernizing their systems to adapt to the digital era, driven by factors such as the need for enhanced customer experiences, operational efficiency, and cybersecurity. This investment is particularly crucial now as the COVID-19 pandemic has accelerated the shift towards digital banking, making it imperative for banks to upgrade their infrastructure to meet evolving customer expectations and stay competitive in the market.

Neobank (2%):

Neobanks are attracting funding as they offer digital-only banking services, leveraging technology to provide innovative solutions to consumers. With lower overhead costs compared to traditional banks, neobanks are appealing to tech-savvy consumers seeking convenient and personalized banking experiences. The current surge in neobank funding is fueled by the increasing smartphone penetration and the growing preference for digital banking services, particularly among younger demographics. This trend is significant as neobanks challenge traditional banking models, fostering innovation and competition in the financial sector, ultimately benefiting consumers with more choices and better services.

WealthTech (8%):

The WealthTech segment is witnessing significant funding as it capitalizes on the increasing wealth and investment opportunities in India. WealthTech platforms leverage technology such as robo-advisors, big data analytics, and AI algorithms to offer personalized investment advice and portfolio management to individuals. The current momentum in WealthTech funding is driven by rising disposable incomes, a growing middle class, and increasing awareness of financial planning and investment opportunities. This trend is essential as WealthTech democratizes access to financial services, empowering individuals to build wealth and achieve their financial goals more efficiently.

InsurTech (8%):

Investment in InsurTech is growing as companies seek to disrupt traditional insurance processes with technology-driven solutions. InsurTech companies utilize IoT, AI, and blockchain to enhance underwriting, claims processing, and risk management, leading to improved efficiency and customer experiences. The current surge in InsurTech funding is fueled by the need for more transparent, affordable, and accessible insurance products, driven by rising insurance penetration and increasing awareness of risk management. This trend is significant as InsurTech innovations promote greater inclusivity and efficiency in the insurance sector, benefiting both insurers and policyholders.

Digital Lending (18%):

Digital lending is attracting substantial funding as it addresses the growing demand for credit, particularly among underserved segments of the population. Digital lenders leverage alternative data sources, AI-based credit scoring, and automated processes to streamline loan origination and decision-making, making credit more accessible and affordable. The current momentum in digital lending funding is driven by the formalization of the informal credit sector, increasing smartphone penetration, and the need for efficient credit solutions. This trend is crucial as digital lending promotes financial inclusion, stimulates economic growth, and reduces reliance on traditional banking systems, especially for underserved segments of the population.

Digital Payment (57%):

Digital payment companies are receiving the majority of FinTech funding in India as cashless transactions continue to rise. Factors such as government initiatives, digitalization of businesses, and changing consumer preferences are driving the adoption of digital payments. Digital payment solutions such as mobile wallets, UPI, and contactless payments offer convenience, security, and efficiency in transactions, leading to their widespread acceptance. The current dominance of digital payment funding is significant as it enhances financial inclusion, transparency, and efficiency in transactions, driving economic growth and reducing reliance on cash-based economies.

In summary, these funding trends reflect the evolving landscape of FinTech in India, driven by technological advancements, changing consumer behavior, and regulatory initiatives. Understanding the reasons behind these trends and their implications is crucial for stakeholders to capitalize on opportunities, drive innovation, and foster sustainable growth in the financial sector.

IBSi FinTech Journal

- Most trusted FinTech journal since 1991

- Digital monthly issue

- 60+ pages of research, analysis, interviews, opinions, and rankings

{kind=link}