Cedar-IBSi FinTech Labs

Cedar-IBSi FinTech Labs

Analyst Briefings

Analyst Briefings

Get in touch

Get in touch

Back

Back

India’s FinTech evolution is moving from payments innovation to data infrastructure

By Venkatesh Krishnamoorti, CEO and Managing Director of Saafe

After a decade focused on transaction rails, the spotlight is now on financial data rails. Account Aggregator represents the next structural leap, enabling programmable credit and smarter financial products powered by verified data.

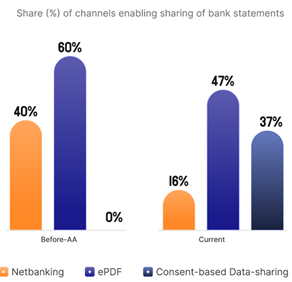

The Consent / Data layer of Digital Public Infrastructure (DPI) is the critical rail for designing & delivering financial services. From a paper/PDF-based source document of financial data to a completely digital form, processes such as profiling, credit assessment, underwriting, up/deep/cross-selling, collection, etc., have become efficient.

Lending:

Real time banking & financial asset data, enabled by AA infra-rails, helps right-sizing of credit. RBI has been consistently nudging CICs to shrink the updation of citizens’ data more frequently. It is currently refreshed fortnightly (earlier it was monthly) and expected to move to “weekly”.

As a lender, it is imperative to be aware of all transactions, including any indebtedness almost real time. Further, financial information sourced via AAs are authentic as they flow from the “Golden record” – Banks, Depositories, RTAs etc.

AA has transformed underwriting processes across the lending landscape. We believe that consent-based data sharing via AA will reach 100% in a year or two, as awareness of data privacy amongst citizens improve and the institutions recognise the substantial savings in time & effort yielded for credit delivery. DPDP Act will also accelerate AA adoption from 2027.

Triangulation/cross-validation of data points sourced independently ensures authentication/verification to eliminate frauds & errors. For eg, GST data (incl. Sales etc) sourced through AA can be verified with the Bank transaction data, also AA-sourced.

With EPFO and ITR as proposed data types to be available on the AA ecosystem in the near future, the availability of all the necessary information for Credit teams will be holistic.

Lenders also have credit products, such as Pre-approved loans, targeting existing customers who have paid their EMIs promptly. Typically, the newer loans are for amounts higher than the previous loans that have run their course. Also, lenders have traditionally relied on “Credit Score” for pre-approvals. However, the score does not help in quantifying the pre-approved loan amount. Relying on financial data (AA-sourced) with a credit score overlay has emerged as the ideal model.

Recurring consents (subject to borrower’s approval, taken for the tenure of the loan) provide rich & relevant insights into the customers’ financials. Borrowers and Lenders benefit from these periodic updates – cross-sell, hyper-personalisation, early-warning, etc.

Wealth management

India is one of the most under-penetrated markets for wealth management. Over the years, Mutual funds through its fixed income and equity schemes have made a significant positive impact. SIPs have grown substantially as a preferred savings/investment option for the average Indian household. However, a lot of ground remains to be covered for instance: Asset allocation as a concept would vastly assist households in managing their investments better in line with their financial goals, whilst managing inflation impact.

Given India’s scale of population and rapidly growing mass-affluent, we believe there will be a wave of automated tools designed & developed for investment advisory & execution. This will be made possible seamlessly with AA-sourced data that will feed into these Robotic investment applications. ML & AI will ensure adherence to the framework at all times, with minimal impact on costs and near-zero manual interventions. Further, fees for such Robotic advisory tools will be very low, making efficient wealth management accessible to all.

In summary, AA’s construct delivering real-time digital financial data has made critical processes such as credit underwriting efficient. The AA industry is working closely with the Financial Regulators and Product manufacturers & distributors to develop innovative use cases that benefit all stakeholders without compromising the data security & privacy of citizens.

Previous Article

IBSi News

Get the IBSi FinTech Journal India Edition

- Insightful Financial Technology News Analysis

- Leadership Interviews from the Indian FinTech Ecosystem

- Expert Perspectives from the Executive Team

- Snapshots of Industry Deals, Events & Insights

- An India FinTech Case Study

- Monthly issues of the iconic global IBSi FinTech Journal

- Attend a webinar hosted by the magazine once during your subscription period

₹200 ₹99*/month

* Discounted Offer for a Limited Period on a 12-month Subscription

IBSi FinTech Journal

- Most trusted FinTech journal since 1991

- Digital monthly issue

- 60+ pages of research, analysis, interviews, opinions, and rankings

- Global coverage

Other Related Blogs

March 04, 2026