Cedar-IBSi FinTech Labs

Cedar-IBSi FinTech Labs

Analyst Briefings

Analyst Briefings

Get in touch

Get in touch

Back

Back

Coronavirus & The Financial Sector: The Co-Relation, Impact & Way Forward

Coronavirus or COVID 19 has triggered an economic collapse globally over the past few months and experts say that the worst is yet to come! Coronavirus has dealt the last nail in the coffin to an economy already burdened with unprecedented debt levels and company valuations.

The stock markets globally have gone into a freefall with major indices falling between 10-20% in the past couple of weeks, with all major countries entering a bear market (>20% decline from 52 week highs). While the biggest losers have been the tourism, aviation, hotels, energy and leisure sectors, the slump in oil prices has sent shockwaves across a global economy that is already staring down the barrel of a meltdown.

This article attempts to dwell deeper into COVID 19’s impact on the financial sector, more specifically the impact on banks, banking technology companies and fintechs.

Banks, the vital cog to any economy, are facing multifold challenges. While the 2008 financial crisis was attributed to sub-prime mortgage loans and the real estate bubble, it is no secret that the 2020 meltdown will be attributed to unprecedented levels of corporate debt. Let’s lay out some of the key challenges:

- Significant downturn in bank valuations driven by plummeting stock prices

- Large drop in transaction volumes among business and retail customers reducing fee and commission incomes

- Pressure on net interest margin, arising from multiple reductions in interest rates by central banks globally

- Adverse impact on credit quality and rising NPAs initially triggered by ‘zombie companies’ and then SMEs. The impact will be magnified by companies operating in ‘code-red’ sectors such as tourism, aviation, leisure, energy and oil and gas which can result in mass bankruptcies, unemployment and negative economic growth

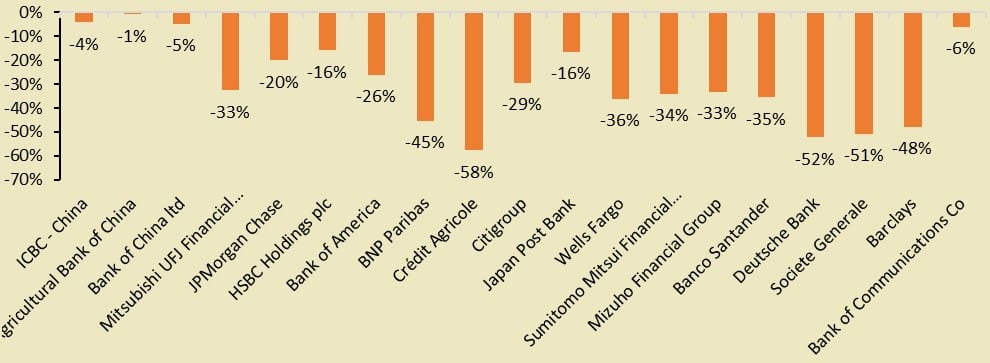

The chart below takes the top 20 banks globally with the exception of China Construction Banking Corp and depicts the total decline in their stock prices over the period 24th February to 13th March 2020.

The average bank stock has declined ~29% over the past 20 days, with the median decline at ~33% and experts fear that this is only the beginning of the colossal damage that lies ahead. The range of the stock price decline is ~57%. Liquidity issues coupled with slowdowns in credit growth and fee income are all set to manifold in the coming days and the situation ahead looks grim to say the least. Regional and country specific trends are becoming apparent as well, for instance, if we were to consider the sharp recovery of the Chinese markets and ignore their numbers, the averages share price decline climbs to ~36% and the median decline inches up to ~34%. The Japanese banks have fallen ~29%, American banks ~28% and worst yet, European banks have fallen a staggering ~48%.

Let’s turn our attention towards banking technology companies and fintechs. While the former is expected to be hit severely, the latter could emerge as a dark horse. FinTechs that provide innovative offerings using digital solutions could potentially emerge as winners. The same can’t be said about banking technology providers running multi-billion dollar technology transformation projects across the globe. Let’s dissect some of their biggest challenges:

- The current business scenario poses a significant risk to current projects in terms of time and cost overruns, project delivery and profitability and in some cases could escalate to project standstills and closures. Banking technology companies globally are plunging into Business Continuity Planning (BCP) mode.

- If substantial risk to current projects wasn’t bad enough, a substantial and adverse impact on revenues going forward is expected as a result of delayed proposal approvals and pipeline conversions, which could topple firms into cost cutting mode

- Team members stranded across the globe and COVID 19 infected teams add up to severe company-wide ramifications and people related liability. Additionally, in light of project delays and closures, unprecedented pay cuts and lay-offs will be seen

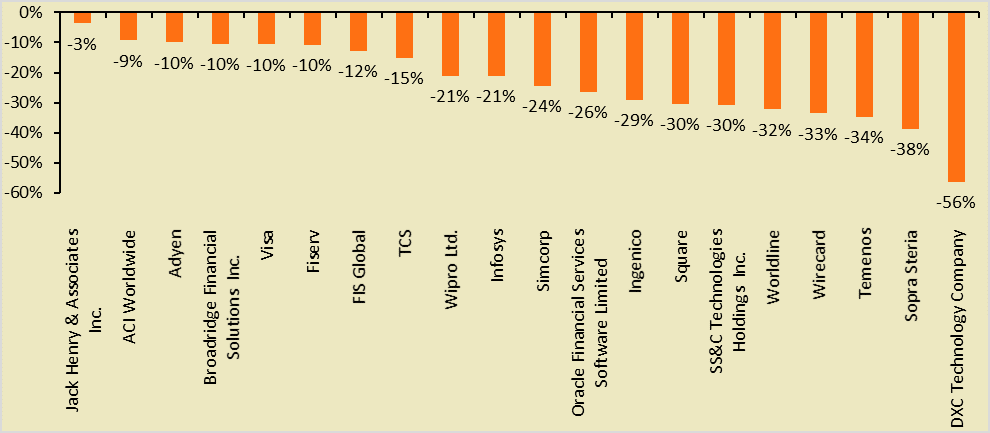

The chart below takes the top 20 banking technology companies and shows the total decline in their stock prices over the period 24th February to 13th March 2020.

The average banking technology stock has declined ~23% over the past 20 days, with the median decline at ~22%. The decline’s range is ~53%. Banking technology companies are yet to see the full impact of project overruns and other risks to on-going large-scale projects, which has sent leading companies into Business Continuity Planning (BCP) mode. American banking technology companies are down ~19% and Indian banking technology companies ~21%. Now, if we were to look at the impact on Europe’s leading banking technology providers, with the exception of Adyen, the average decline inches up all the way to ~32%.

At this stage, the global outlook looks forlorn with most leading investment houses predicting a US and EU recession by July 2020 and many fearing that it is already here. However, even these treacherous times present some opportunities for banks, banking technology companies and fintechs.

Banks with surplus capital, a strong balance sheet and end to end digital services stand to emerge as winners in the medium to long term. In the immediate term, banks will look at end to end digitization in a lean and fast-tracked manner to ensure that all products and services can be accessed digitally. Already 72% of UK consumers and 62% of US consumers carry out majority of their banking online and these numbers are only set to rise globally given the restrictions and lockdowns enforced globally. Banks will look at strategic branch consolidations and branch closures to save costs and resort to pay cuts and layoffs where necessary. Challenger banks with a full gamut of digital services and digital only models could emerge as winners based on how they harness the opportunity and how quickly they can onboard new customers and up-sell, cross-sell existing customers.

Banking Technology companies with a proven track record in cloud-based delivery (SaaS solutions) and offshore services could emerge as winners among the losers. These are primarily banking technology companies that have rode the paradigm shift towards microservices based architecture from a modular architecture which facilitates the effective deployment of cloud-based solutions. Secondly, banking technology companies will be able to answer the vital question; Does remote working work? If so, it could bring down costs significantly, transform the business model and improve bottom lines for companies globally. Lastly, long term opportunities through deferred up-sell, cross-sell and collaborations exist for companies that continuously exceed client expectations and deliver projects effectively.

It’s a mixed bag for fintechs really. Funding is set to dry up significantly after a stellar 2019 wherein fintech funding climbing to ~$100 Bn. However, fintechs with targeted product offerings such as early payrolls, chatbots and contactless payments through digital platforms will continue to standout. Cloud-based banking suppliers like Mambu, Thought Machine, nCino and Leveris can emerge as winners. Additionally, banks would be more willing to work with agile fintechs now more than ever before as they look at targeted solutions from fintechs in the leanest, quickest and most cost-effective for their short-term fixes and transformations.

One thing is for sure, a daunting 2020 beholds with many challenges and some opportunities!

Written By,

Sooraj Mehta

Cedar Management Consulting International

IBSi News

Get the IBSi FinTech Journal India Edition

- Insightful Financial Technology News Analysis

- Leadership Interviews from the Indian FinTech Ecosystem

- Expert Perspectives from the Executive Team

- Snapshots of Industry Deals, Events & Insights

- An India FinTech Case Study

- Monthly issues of the iconic global IBSi FinTech Journal

- Attend a webinar hosted by the magazine once during your subscription period

₹200 ₹99*/month

* Discounted Offer for a Limited Period on a 12-month Subscription

IBSi FinTech Journal

- Most trusted FinTech journal since 1991

- Digital monthly issue

- 60+ pages of research, analysis, interviews, opinions, and rankings

Other Related Blogs

November 28, 2025

Modernising core systems in financial services without a complete overhaul

Read MoreOctober 22, 2025